Articles

Africa’s Leapfrog into Stablecoins & Borderless Banking

Kayla Phillips

June 24, 2026

As stablecoins rapidly reshape our global financial system, the ‘digital dollarization’ narrative has largely focused on Latin America’s inflation-prone economies and Southeast Asia’s high-velocity remittance corridors – often overlooking Africa’s immense potential.

Africa represents the ultimate leapfrog opportunity: a region with a young, digitally-native, and largely unbanked population that’s not just waiting for better banking, but actively bypassing legacy infrastructure to adopt borderless, stablecoin-first financial services at record speed.

Africa’s Vast yet Challenging Fintech Market

Africa is a massive but historically challenging market for fintech, offering significant payoff for companies that can successfully navigate its challenges and scale effectively. African B2B payments make up a $1.5T market, growing 15% per year. Within this, cross-border payments total $500B TPV and $45B in fee revenue, growing 20-25% per year.

However, friction remains high due to a range of factors: local currency instability, a large unbanked population (52%), insufficient financial infrastructure to support local and global business, and the world’s highest cross-border payments fees (9% vs 6% global avg). Today, 80%+ of intra-African cross-border payments settle in USD or EUR because inadequate intra-African payment infrastructure necessitates routing through foreign banks – yet only 5% of African businesses have access to USD banking rails.

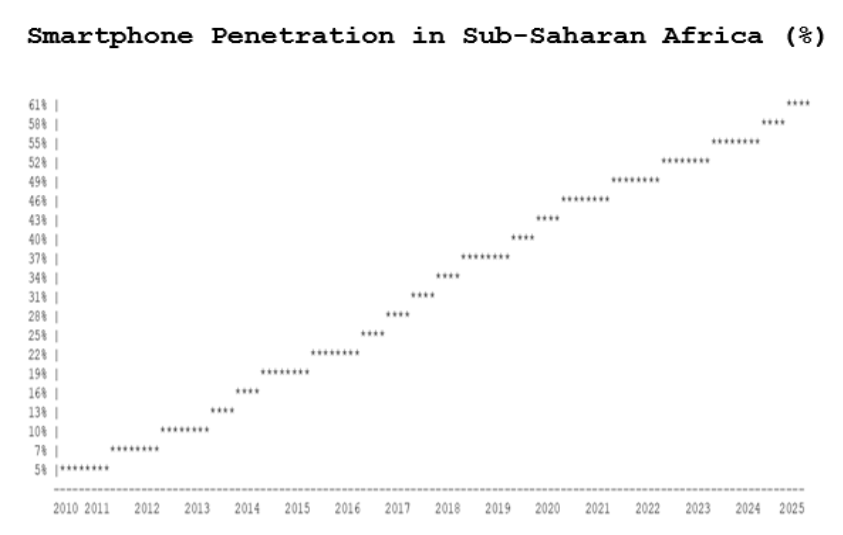

The Smartphone Adoption Precedent

Over the past 10-15 years, widespread smartphone adoption has transformed Africa into a mobile-first, globally connected continent, significantly boosting quality of life and economic growth. Smartphone penetration in Sub-Saharan Africa is projected to reach 87% by 2030, already contributing to 8.1% GDP growth in 2022.

While Africa’s smartphone adoption began a decade later than developed economies, what’s remarkable about its rapid growth is that Africans bypassed desktop computers, landline phones, and the physical infrastructure needed for these technologies, instead leapfrogging straight into smartphone adoption. Adoption has surged out of necessity as more industries digitize. Other drivers include Africa’s young (median age of 19), tech-forward population and falling smartphone prices. Adoption has unlocked entirely new markets, connecting hundreds of millions to the digital economy in record time.

The Stablecoin Adoption Paradigm

With African smartphone penetration expected to reach 67% this year, the foundation is set for the continent’s next mobile-first tech wave.

Just as smartphones enabled Africa to leapfrog into mobile internet connectivity over the last decade, stablecoins are now powering a similar jump into modern, borderless financial services at a faster rate than the rest of the world.

Like smartphone adoption, stablecoin adoption is surging out of necessity – to protect against local currency instability, bypass outdated traditional financial rails, and enable access to global business opportunities.

African Fintech’s Inflection Point

Several trends are reason to believe that the next 5-10 yrs of African fintech will be a giant leap forward from the last 5-10 years:

- Skyrocketing Adoption: Africa is experiencing the fastest rate of fintech and crypto adoption in the world – a trend expected to continue through 2030. Crypto adoption has grown 25x since 2021, while fintech is expected to grow 13x from 2023 to 2030. Drivers include rapid smartphone adoption, digital infrastructure improvements, a young and digitally-native population, and widespread underbanking.

- Fintech Investment & IPOs: Africa’s largest fintechs are maturing, with over a dozen $1B+ fintech companies, including 3 public and 3 eyeing IPOs in the next 1-3 years. Global capital is pouring in, with major players including Visa, Mastercard, PayPal, Nubank, Google, Coinbase, Binance, and Tether making recent headlines for ramping up their African fintech investment and expansion efforts.

- Pro-Crypto Regulation: Nigeria, Kenya, South Africa, and Ghana are formalizing their digital asset regulatory frameworks and beginning to issue VASP licenses to crypto firms.

- Economic Reform & Global Investment: Broader economic reforms and initiatives across Africa are fueling economic activity and global investment in the region. The recent Pan-African trade agreement AfCFTA, instant payments system PAPSS, and growing infrastructure investment from China, India, Europe, and US are all driving greater demand for seamless cross-border payments with instant settlement.

The Need for Borderless, Stablecoin-first Banking

These tailwinds set the stage for a new chapter of growth in African fintech, but they also reveal gaps in the market that need to be filled. One such gap is the need for mobile-first neobanking services that enable local African businesses to easily transact with partners locally and abroad.

Enter our newest portfolio company, Daya. Daya is an African stablecoin neobank, providing local businesses with virtual USD bank accounts, instant global payments, payment cards, and robust financial services through a sleek mobile app. Daya’s founding team are Nigerian natives who previously built Helicarrier, one of Nigeria’s earliest crypto remittance platforms. Their innate understanding of the local market, crypto and fintech domain expertise, and regulatory-first approach under a licensing regime that favors local upstarts over global incumbents make a compelling case for Daya’s bright future.

Conclusion

At Hivemind, we envision a future global financial system run on blockchain rails and we invest in the builders making this a reality. We see Daya as the gateway for African businesses to access the global dollar economy, transforming the historically underserved African market into a global economic hub run on modern financial infrastructure. Our team is actively investing in opportunities across market infrastructure, payments, and stablecoins aligned with this thesis, and we are always looking to connect with founders building innovative solutions in this space.

-

DISCLAIMER: All views expressed are Hivemind’s own views. The information provided herein has been produced and issued by Hivemind Capital Partners UK LLP and/or Hivemind Capital Partners LLC (“Hivemind”) and is being provided for informational purposes only. This document is not to be distributed or reproduced in any way. This document does not constitute or contain an offer to purchase or sell securities. This document is confidential and intended for the person to whom this was delivered. If you have not received this document from Hivemind you are hereby notified that you have received it from a non-authorized source and you are prohibited from reading, using, retaining, disseminating or copying this material without the prior express written consent of Hivemind. Neither Hivemind nor any of its affiliates or representatives makes any representation or warranty, express or implied, as to the accuracy or completeness of the information contained herein or any other written or oral communication transmitted or made to the recipient. The information contained in this document is current as of the date indicated, and Hivemind undertakes no obligation to update, modify or amend this document or to otherwise notify a reader in the event that any matter stated herein changes or subsequently becomes inaccurate.

This document has not been compiled, reviewed, or audited by an independent accountant. Past performance should not be construed as an indicator of future results, and there can be no assurance that historical trends will continue. This document does not include information regarding each investment or investment strategy pursued by the Funds. References to investments included herein should not be construed as a recommendation of any particular investment.

Certain information contained herein may constitute “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof, other variations thereon or comparable terminology. All such forward-looking statements are solely statements of opinion, and there is no assurance that they will be predictive of actual events.