Articles

Winter?

October 5, 2022

One reality of institutional-grade asset management is having to deal with the complexity of correlations between market movements, market sentiment, and market commentary. Volatility is not necessarily a bad thing, nor are bear markets or asset-class declines; though the press and popular opinion may often suggest otherwise.

The fact is, however, that even emotion-free investing is still complicated by swings in human opinion. Put more simply, what does it mean for Hivemind that in the second quarter of our existence as an asset manager, we (by all accounts) entered a punishing and destructive crypto “winter?” As participants across the entire class of digital assets, we are frequently asked some version of that question. As such, below I offer some perspective on these issues - and related concerns - about crypto’s future.

First, though, we’ve already written elsewhere about what we’re building here at Hivemind and our general perspective on web3, blockchain and digital assets. With that as a backdrop, here are some ways we think specifically about the declines in both crypto and traditional asset classes over the past 6-8 months:

Quantity doesn’t necessarily mean quality

It goes without saying that crypto is newsworthy, for better or worse - and when crypto declines, it quickly creates headlines; especially given the high level of retail interest and exposure, as well as the high level of visibility relative to traditional (aka “boring”) financial products. Overall, of the thousands of articles written on the sector of late, most were negative in sentiment and reflected a persistent zeitgeist that if crypto isn’t a fad, it should be. The volume of this noise, however, isn’t necessarily reflective of quality of insight. So rather than list out dozens of examples of off-base commentary, we’d instead point to pieces like this summary on financial content curator Nerdwallet as positive exceptions to what often looks like pretty slanted commentary. Neither of these pieces reflects crypto-zealotry. Instead, they take a measured, high-level view of both the spaces challenges and opportunities. That view aligns far more closely with our own than with the mass of mainstream coverage.

The long view matters

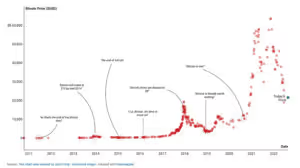

Hivemind was built on a belief in the long-term, enduring value that will be created by innovations in blockchain technology. Unsurprisingly, this view is one that is not universally accepted (yet?) and welcomes critique - especially in down markets. For disruptive technologies in general, and crypto in particular, this is nothing new. A good depiction of this behavior can be seen at this clever site, (screenshot below), which charts bitcoin’s price against anti-bitcoin commentary. Even with the recent falloff, it’s obvious that over the past decade-plus, that one currency repeatedly has proven doomsayers wrong. While this itself is not a justification for investing, nor an apologia for crypto’s excesses, it is cause to be skeptical of the skeptics. Those who folded at the first sign of negative bitcoin commentary would have sacrificed astronomical returns over the proceeding years. The long view matters.

Timing is everything ( and overleveraging is always risky, regardless of asset class)

More broadly than bitcoin, we’ve seen a pandemic-driven, supply-chain-compromised, inflationary environment wreak havoc with almost all financial markets worldwide. As destructive to value as this moment in time has been relative to previous highs, it has also created a plethora of investment opportunities, for the right teams with the right background and resources.

Hivemind’s general view here is that we’re seeing a significant value correction in terms of pricing, and have shifted some of our asset allocation accordingly, to take advantage of these moves. Further, due to our multi-strategy approach, we’re not subject to short-term time horizons that limit our ability to participate across markets, nor are we subject to liquidity or margin issues. This presents both compelling opportunities, as well as the ability to capitalize on them.

Net-net, while there have been some troubling failures of both firms and of assets, we do not see those as indicators of a lack of integrity in crypto overall. As others have documented, many of the platform collapses had involved overleverage, which is a risk across traditional capital markets and even personal finance, and clearly not limited just to crypto. Distinctions about whether or not traditional finance platforms could have leveraged themselves as much as Three Arrows seems like splitting hairs.

To be clear: we are not dismissing the massive paper (and realized) losses in markets, crypto and otherwise, over the last year. We simply are saying that these value shocks - however anecdotally dramatic - may have just expanded our opportunity set more dramatically than we ever could have hoped.