Articles

How Tokenization Changes Asset Management

Richard Skeet

July 8, 2026

"Tokenisation is emerging as one of the transformative forces in modern finance." – Nelson Chow - HKMA.

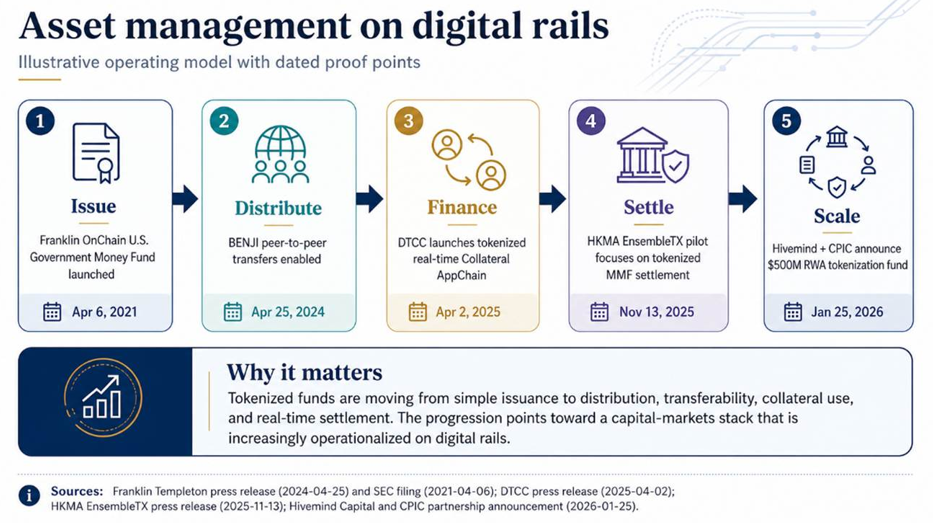

Tokenization matters when a fund share starts acting like working inventory, not a static wrapper. A money fund, Treasury sleeve, private credit instrument, or real-asset product that lives onchain can reach more investors, move across jurisdictions more cleanly, and do more inside financing and collateral workflows. Franklin Templeton’s onchain government money fund reported $843.74 million in net assets as of March 31, 2026, and the firm said assets across its Benji platform were nearing $1.5 billion in late March. That is enough to treat tokenized funds as live market structure.

Distribution is where the business model starts to change. Franklin enabled peer-to-peer transfers for eligible holders of that fund in 2024, which meant a regulated money market fund share could move directly between approved investors on public blockchain rails. That is more than just a product feature. It widens the addressable buyer base and strips friction out of how capital reaches the product. BlackRock's 2026 product outlook points the same way, describing tokenization as part of a wider expansion of the investible universe and a bridge between traditional and digital markets.

Distribution may prove to be the real fault line. The gaming industry offers a useful analogy: many of the largest pools of value did not come from better content alone, but from better routes to the user. Steam changed PC game discovery and monetization. Mobile app stores turned casual access into the largest gaming segment, with Newzoo estimating mobile gaming at $92.6 billion, or 49% of global games revenue, in 2024. More recently, Bain noted that top-grossing mobile games have increasingly built their own direct stores, with the share rising from 12% to 44% over five years as publishers try to own more of the customer relationship and avoid platform leakage. The lesson for asset management is not that funds become games. It is that distribution architecture compounds. Managers that control more of issuance, access, transferability, collateral use, and lifecycle management should capture more of the economics than managers who only manufacture the product.

Collateral is where the commercial payoff gets harder to ignore. DTCC's current work is aimed at a simple problem: too much inventory is still slow to move, hard to finance, and trapped inside fragmented systems. Its Collateral AppChain is built to let institutions tokenize assets using any tokenization capability and use assets issued on public or private networks while staying connected to traditional market infrastructure. DTCC's launch language goes further, tying the platform to greater collateral mobility and velocity, better capital efficiency and liquidity, and a broader digital liquidity pool. That is where tokenized fund shares stop being a distribution story and start becoming better treasury assets, better funding assets, and more useful portfolio tools. The same logic extends into private credit, where a cleaner transfer stack and better collateral utility can widen access while making the asset itself easier to finance and monitor after issuance.

Th elegal claim still has to travel with the token. The SEC’s January statement matters because it draws a line between issuer-sponsored tokenized securities and third-party structures, including custodial and synthetic forms. Those categories do not all give investors the same rights, and some leave the holder exposed to an intermediary rather than the underlying asset itself. Asset managers can work with new rails. They still need clean ownership and clean entitlements.

Asia is where this starts to look like an operating model rather than an idea. Hong Kong’s Project Ensemble moved into pilot phase in November 2025 with an initial focus on tokenized money market fund transactions and real-time liquidity and treasury management. In March, the HKMA said EnsembleTX had already entered real-value transactions involving tokenized deposits and digital assets, with more banks and more use cases to follow in 2026. That is one reason our January partnership with CPIC IMHK matters. The strategy, with an initial target capacity of up to $500 million, pairs our digital-asset market structure and operations experience with CPIC IMHK's regulated distribution and institutional network in Hong Kong.

The post-trade stack is starting to meet the product. DTCC said in December that DTC had received SEC no-action relief to offer a controlled-production tokenization service for select DTC-custodied assets, with rollout anticipated in the second half of 2026. DTCC says the digital form is intended to carry the same ownership rights, investor protections, and economic entitlements as the traditional asset, and the initial set includes highly liquid equities, ETFs, and U.S. Treasuries. That is how tokenization moves out of sidecars and into the market's core machinery.

Tokenization broadens the market by changing the operating model of asset management itself. The first wave was wrappers. We believe the next wave is funds, cash products, private credit, and real assets that can be issued, distributed, financed, and posted as collateral without losing legal clarity.

-