Articles

Livepeer Governance Proposal – The Department of Livepeer Efficiency

November 18, 2024

Summary

- We believe Livepeer have one of the most commercial offerings within the AI space, with clear product market fit, albeit with revenues at an early stage.

- LPT trades at a significant valuation discount to mid-large cap AI peers, which we feel is unjustified

- We believe the key issue is the excessively high inflation rate which results in $80m of supply annually, much of which is sold on exchange by orchestrators looking to monetize yield for income.

- This supply/demand imbalance has severely curtailed the LPT price in recent months/ years

- We believe the staking design/ parameters could be dramatically optimised, in a way that leaves orchestrators with adequate compensation for operating infrastructure (and assumes some level of consolidation) whilst dramatically improving the supply/demand of the LPT token

Introduction

Amongst the subset of AI projects, we believe Livepeer has one of the most compelling commercial offerings. Transcoding is a $20bn+ market, growing at >20% CAGR and Livepeer has clear product market fit, offering ~90% savings vs GPU cloud providers. Revenues are still small ($300k pa) but are improving and the recent launch of the AI subnet significantly improved revenues on its launch in late Q3. The team are heavily focused on scaling the AI subnet and have a number of startups actively building on it.

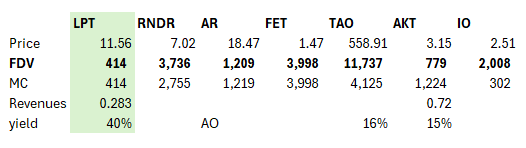

While revenues across the sector are frankly embryonic, Livepeer is one of the strongest projects for actual revenue generation, as shown below. Yet in terms of valuation, LPT is very much at the low end of the pack, with peers trading at 3-10x LPT on a fully diluted basis.

We need to talk about staking

We believe the problem lies in its staking model. In summary

- The model is designed to encourage a 50% staking rate. Above 50%, the yield falls by X% per [epoch], below 50% and the yield increases by X%. However, there appears to be no specific justification as to why 50% of tokens need to be staked.

- This results in a ~50% yield at the 50% staked equilibrium level. There is little stated reason for yield to be this high, as we discuss below

- Delegators stake with orchestrators (ie validators) who take a cut of both the fee and inflationary staking revenue (this varies but on average ~X and 15% respectively)

- Since revenues are currently limited, orchestrators understandably need to be compensated with token inflation to supply the network with infrastructure for transcoding and AI jobs. We think this is reasonable and a critical part of bootstrapping the supply side of a platform business. But we think this incentive structure is extremely inefficient and has resulted in excessive supply side capacity.

- With 50% of the circulating supply staked (currently X%) and circulating market cap = FDV since the token is fully vested, this equates to ~20% inflation per year.

As one might expect, much of this yield is sold directly onto exchange to provide orchestrators with yield (here an example of a large either orchestrator or delegator selling $100k onto Okex). As there is currently limited natural demand for the token other than investment/ speculation, this results in a significant supply/demand imbalance.

Over the past year we have seen support at ~$9-11 but on any pump, there is significant resistance and we believe this is likely stakers looking to offload their yield at locally attractive levels. In short, the token can’t pump and as we can see from the chart below it has been one of the weakest performers on a 2 year and recent basis.

We believe that a yield of 10-20% would be more than adequate for orchestrators to remain committed to the network (yields for RENDER validators are X% and there is anecdotally plenty of capacity).

To illustrate this, let’s consider the profitability of orchestrator set. Based on our conversations with management we understand or have made educated guesses for the following

There are 100 orchestrator slots, 70 of which are active

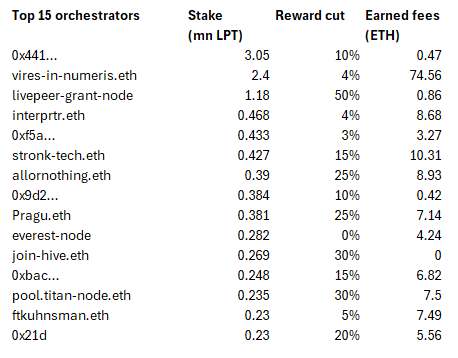

- The average take rate on inflationary yield is around 15% (varies from 0 to 30%, but average 16% across top 15)

- Many of the orchestrators also own sizeable holdings and likely own ~25% of total staked LPT

- Costs range from an initial investment of ~$10k with an annual expense of $1k/month for smaller orchestrators, to $100k+ investment with annual costs of ~$200k+

On that basis, the average orchestrator earns ~$200k pa. As you can see from our estimates below, we believe large and small validators are currently operating at a significant profit margin (>50%). Furthermore, given the current level of activity on the network, it appears there is significant excess capacity and we can see this in the table below, in that the average top 15 validator has earned ~10 ETH since the migration to Arbitrum One (2022).

Our proposal

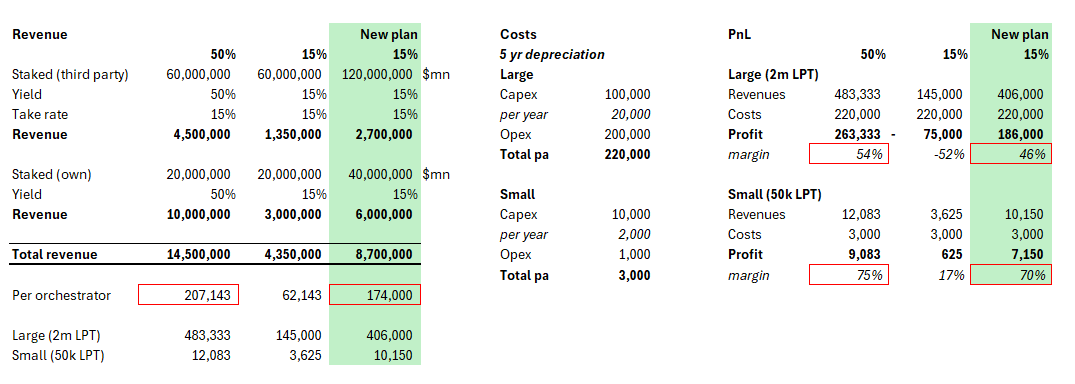

We believe that cutting the yield to 15% will result in the majority of orchestrators remaining in profit but will likely lead to a degree of consolidation (which will increase the yield for those that remain). In time, as underlying activity increases (and with it, fee revenue), the supply side should also expand but for now the excess (inflation funded) supply base serves little economic purpose and is pointlessly dilutive to existing investors.

However, we believe that the 70% reduction in annual token inflation will have a dramatic impact on the price of LPT and given the valuation discrepancy vs peers, we think it is reasonable to assume the price doubles under this proposal (which would still leave it as the cheapest major AI project in the peer group above, on an FDV basis). Similarly, we assume a reduction in orchestrators from 70 to 50 due to consolidation. The net impact significantly offsets the reduction in revenue as we can see in the ‘New plan 15%’ column. As such, we believe most validators will still remain profitable.

Conclusion

We believe Livepeer is an innovative project with genuine product market fit, that is being held back by poorly designed tokenomics. Our proposal would be significantly accretive to investors given the change in supply/demand dynamics and only marginally dilutive to orchestrators, many of whom are significant LPT holders themselves and would therefore benefit from a material offsetting impact from a revaluation in their LPT holdings. We welcome your feedback.

- Hivemind Capital Liquid Trading Team